A HISTORY OF DISCIPLINED INVESTING

Volatile Markets. Enduring Principles.

From the dot-com crash of 2000 to the financial crisis of 2008, we have helped our clients navigate bubbles, volatility, and uncertainty. Today’s market challenges carry a familiar tone – echoing past cycles of excess and speculation. Just as before, our disciplined, risk-aware approach is built to help guide our clients through uncertainty.

WHY CHOOSE HEMISPHERE?

- Three Decades of Trust - Serving individuals, families, businesses, and charities across Canada for over 30 years.

- Independent Advice - We are not tied to any institution or product. Our only priority is what is best for you.

- Direct Portfolio Management - You work directly with your portfolio manager — no intermediaries.

- Fiduciary Duty - As registered portfolio managers, we are legally bound to act in your best interest.

- Customized Portfolios - Your portfolio is built around your specific goals and constraints.

- Transparent Investments - We focus on high-quality, publicly-traded securities — not illiquid or opaque alternatives.

- Competitive Fees - Our fees are based on assets under management and are clearly disclosed.

- Clear Reporting - We report performance net of fees using a Time-Weighted Rate of Return (TWRR).

- Segregated Assets - Your assets are held with our custodian, National Bank, and are fully segregated under your name.

- Tax-Efficient Strategies - We optimize security placement to minimize your overall tax burden.

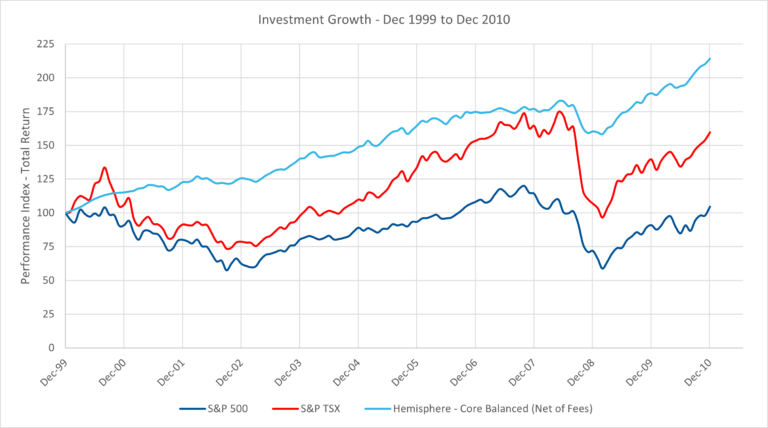

A LOOK INTO THE PAST

Toward the end of the 20th century, investor optimism was running high. U.S. stocks had delivered outsized returns throughout the 1990s — one of the best decades in market history. This performance lured many investors into the market. But by late 1999, valuations had reached historic highs, and stocks had simply become too expensive. The optimism quickly unraveled.

In early 2000, the dot-com bubble burst, wiping out trillions in market value almost overnight. Technology stocks, which had soared on hype and speculative capital rather than profits, collapsed. Investor confidence was shaken, and the broader economy slipped into recession shortly after.

Responding to this collapse, the U.S. Federal Reserve aggressively cut short-term rates in 2002 and held short rates at this level for many years. By 2007 these ultra low rates, combined with easy credit, lax mortgage standards, complex securitized financial instruments and irresponsible rating agencies, created further bubbles in real estate, mortgage securities, stocks, commodities, derivatives, and even outright fraud. Greed and negligence infected the investment and banking communities. This bubble eventually burst in 2008.

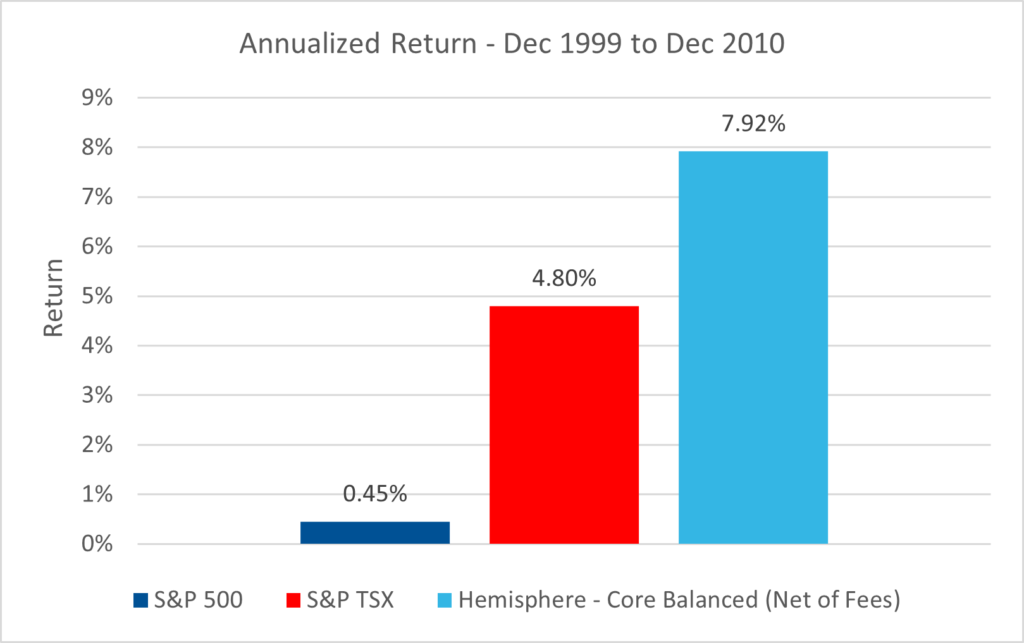

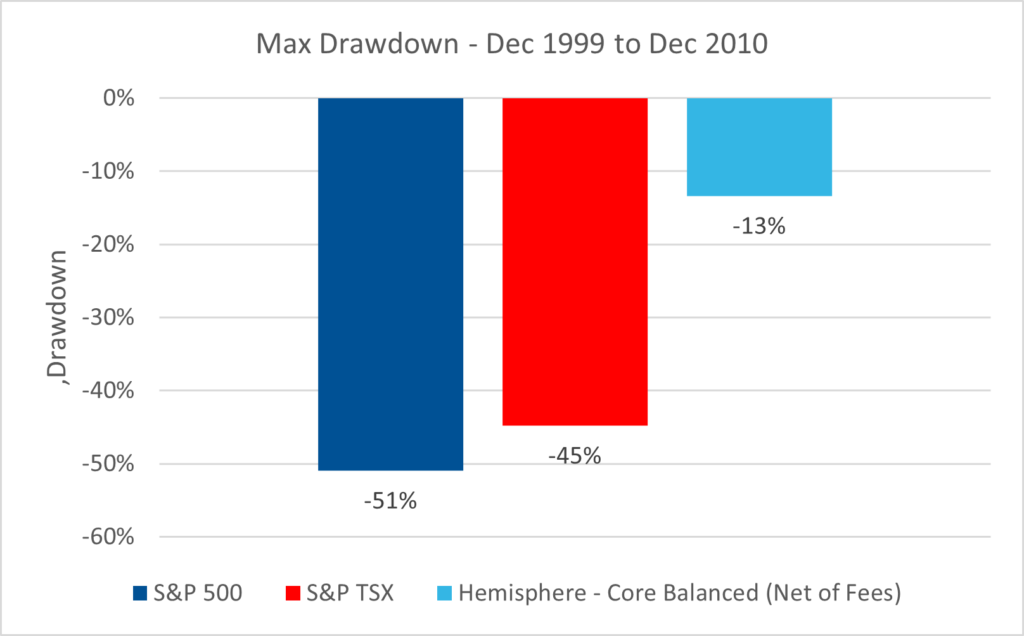

This decade of bubbles produced dismal returns for investors. The U.S. stock market posted its worst performance for any calendar decade in nearly 200 years. Canadian markets did somewhat better but also suffered significant drawdowns and produced meagre returns.

During this period, many investors learned the hard way about how difficult it is to rebuild a retirement portfolio after substantive capital losses, especially with cash flow needs. Unfortunately, bailouts are for banks, brokers and car manufacturers – not individual investors.

HOW WE PERFORMED

Our returns over the decade following the dot-com bust were solidly positive. More importantly, these returns were achieved without the violent downside swings encountered in the stock market, allowing us to comfortably support our clients’ cash flow needs. The risks we took were modest, because we have no incentive to take foolish risks with our clients’ wealth. Our results were built on:

Remaining vigilant

Proactive risk management

Focusing on fundamentals and valuations

Disciplined security selection

Avoiding speculative mania

Our approach has continued to help our clients safeguard their wealth during periods of market weakness. We believe it remains just as relevant today.

*The Core Balanced Composite consists of consolidated client portfolios with an equity mix between 40% and 80%. These are considered moderate to higher risk portfolios.

THE CURRENT INVESTMENT ENVIRONMENT

Today’s investors face a storm of instability that bears similarities to past cycles. Just like in the late-1990s and mid-2000s, we are seeing the return of investor behaviour that is focused on short-term gains over long-term prudence. Excess enthusiasm, distorted incentives, and a rush for quick returns risks leading to the same destination as past cycles – a painful repricing.

Tariffs And Trade Wars

Trade tensions and tariffs are undermining global supply chains and threatening trade wars. Higher tariff costs will ultimately be absorbed by consumers, corporations or both. The result? Rising prices and pressure on corporate profit margins.

Geopolitical Instability

Geopolitical conflicts are increasing in frequency and intensity. From military confrontations to economic sanctions and fractured alliances, these developments introduce structural uncertainty and raise the risk of unexpected “tail risk” events that can shock global markets.

Artificial Intelligence (AI)

AI hype has triggered a wave of excitement and spending. Many companies are investing heavily in AI infrastructure but revenue has not yet materialized to match. Capital expenditures are surging, free cash flow is shrinking, and the risk of overcapacity looms.

Stock Market Valuations

Stock market valuations remain elevated, reflecting a level of optimism that appears disconnected from macroeconomic and geopolitical reality. With high expectations already baked in, any disappointment in earnings or growth could lead to swift repricing.

Speculative Investments

Speculative investments have been resurfacing, reminiscent of past bubbles. From private investments to meme stocks, investor capital continues to flow into high-risk corners of the market. In many cases, fundamentals have taken a backseat to narrative and momentum.

Cryptocurrencies

Cryptocurrencies remain a volatile and largely unregulated asset class. Crypto markets have become large enough that any weakness or malfeasance could have a contagion effect.

Elevated Debt Levels

Government debt levels continue to mount. Despite higher interest rates, borrowing has not meaningfully slowed. This creates long-term headwinds for economic growth and increases the potential for debt-related crises if liquidity dries up.

Investor Complacency

High valuations and tight credit spreads on fixed income investments suggest complacency. Investors are being paid very little extra to take on additional risk.

OUR APPROACH IS BUILT FOR TIMES LIKE THESE

When markets are expensive, and economic signals are mixed, we believe our most valuable attributes are our independence and our ability to move away from the herd. Many advisors talk about the “career risk” from ignoring specific investments due to the risk of underperforming in the short-term. As an independent firm, we do not need to cave to these pressures. This “career-risk” is not part of our decision-making process. When risk is rising, objectivity and flexibility matter more than ever.

One of the most enduring lessons of investing is that the price you pay ultimately influences your long-term return. Markets today are priced for a near-perfect future – soft landings, falling inflation, continuous innovation, and geopolitical stability. Though a possibility, it is a lot to ask for in the current environment.

In this environment, capital preservation is not about avoiding opportunity — it is about being prepared for better ones.

The AI revolution may well be real, as the internet was. But history shows us that investing through hype requires clarity, selectivity, and patience. The early winners of the dot-com era were generally not those that thrived in the long-run. Our approach is to avoid the hype and continue to invest in stable companies that will generate value — not just headlines — over the next decade.

WE DON'T OWN THE MARKET

Real investing is about having a long-term strategy that withstands cycles — and the discipline to follow it. We recognize the importance of staying invested. Though the market as a whole may be expensive, there are always opportunities – it is simply a matter of identifying them. Our security selection process means we don’t own the market, and can work to identify these opportunities.

We believe the next phase of the market cycle will reward patient, fundamentals-driven investors. As ever, we remain committed to our investment fundamentals:

MAXIMIZING LONG-TERM NET WORTH

We are not market timers. Successful investment management is about effective asset allocation over the long-term between equities and fixed income.

INVESTING WITH A MARGIN OF SAFETY

Our conservatism means we would rather be reasonably certain of a good result than hopeful of a great one. Good investing is about avoiding mistakes.

DISCIPLINED APPROACH

Conviction in our insight and decision-making approach facilitates the framework to successful and reliable investment management.

VALUE INVESTING

Our business is one of identifying undervalue in the financial markets. We want to own good companies, but at the right price.

INDEPENDENCE OF THOUGHT

We think for ourselves. Other business interests, recent investment returns and consensus views do not shape our investment management approach.

The old adage is that “As long as the music is playing, you’ve got to get up and dance.” Fortunately, we are not very good dancers and prefer to keep our footing.