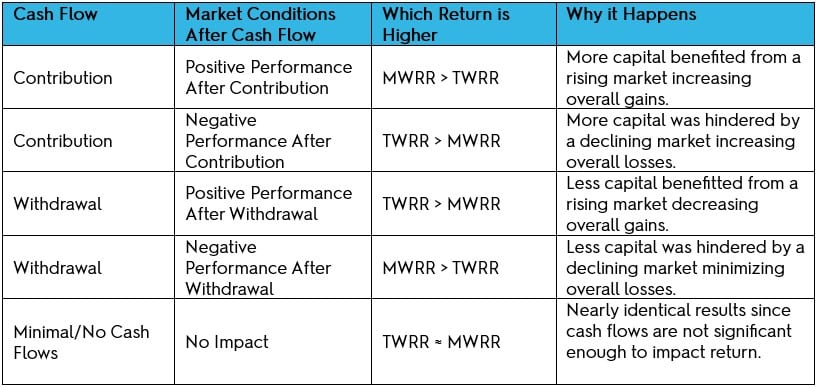

The table below outlines common scenarios where the MWRR is typically higher or lower than TWRR over shorter time periods. This is dependent upon the timing of cash flows relative to market performance.

Imagine three investors – Investors A, B and C – each starting with $50,000 in their portfolios on January 1. Their portfolios are managed by Financial Advisor 1.

- Investor A does not touch their portfolio all year.

- Investor B withdraws $10,000 on July 1 for some personal expenses.

- Investor C receives a mid-year bonus and deposits an additional $10,000 on July 1.

Their quarterly returns are:

- Q1 +3%

- Q2 –4%

- Q3 +6%

- Q4 +5%

We can calculate the performance for this group of investors as shown in the table below:

Calculation Notes

The TWRR is calculated by linking the period’s return between each cash flow. Since all cash flows occur at the start of a quarter, we can link each quarter’s return:

(1+0.03) × (1−0.04) × (1+0.06) × (1+0.05) −1 = 11.65%

The MWRR uses the internal rate of return formula in Excel (XIRR), accounting for the exact timing and amounts of cash flows to solve for the MWRR formula previously shown.

Now assume there are Investors D, E and F who start with the same initial investment and have the same cash flows, but work with Financial Advisor 2.

Their quarterly returns differ from investors A, B, and C as shown below:

- Q2 +2%

- Q2 –2%

- Q3 +5%

- Q4 +4%

We can calculate the performance for the second group of investors as follows:

If we were to compare the MWRR between both groups of investors, we might conclude that Investor F performed similarly to Investor A and outperformed Investor B. We might then conclude that the performance of the two financial advisors varied with each individual investor and that one financial advisor did not necessarily outperform the other.

However, if we compare the TWRR – which excludes the effects of cash flows – it is clear that the performance of Financial Advisor 1 exceeded that of Financial Advisor 2 over the selected period.

It should be noted that while looking at time-weighted performance is a more appropriate comparison, simply looking at performance is a simplistic analysis when evaluating a financial advisor. It is also important to try and understand what caused the difference in performance. Investors D, E and F suffered a smaller drawdown in Q2 so it is possible that Financial Advisor 2 was taking less risk and had lower returns as a result.