When deciding whether it is better to pay off the mortgage or invest, it is important to understand the expected rates of return for each option.

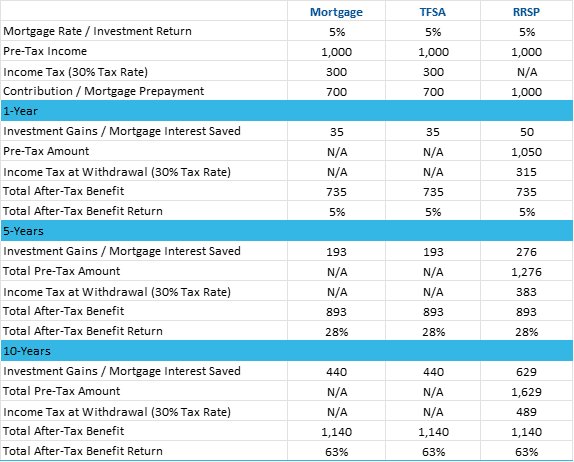

We can start by considering the scenario where your mortgage rate is equal to your investment return in a TFSA or RRSP. For example, if you have a mortgage rate of 5% and expect to earn a 5% return in your TFSA or RRSP, the financial outcomes of both strategies are essentially the same in terms of the overall benefit.

The difference, however, lies in how you expect to achieve the 5% return. In the current interest-rate environment, it is unlikely that a TFSA or RRSP could achieve a 5% return without higher-risk fixed income or equity (stock) exposure. This means that your TFSA or RRSP investments will likely have more risk than paying off your mortgage. This also means that your investments will tend to have more volatility and your return could be higher or lower than 5%.

If your return expectations for a TFSA or RRSP are higher than your mortgage rate, investing may be more appealing than paying down your mortgage – though higher return expectations typically mean higher-risk investments.

As shown in the table above, TFSA contributions and mortgage prepayments are made with after-tax dollars and are easy to compare. RRSP contributions are, in theory, made with pre-tax dollars so the amount initially contributed should be more and is subsequently reduced by taxes when withdrawn. In reality, most people make an RRSP contribution with after-tax dollars and expect a refund after filing their taxes. The refund would therefore need to be contributed to the RRSP as well to reflect the full pre-tax dollar contribution.

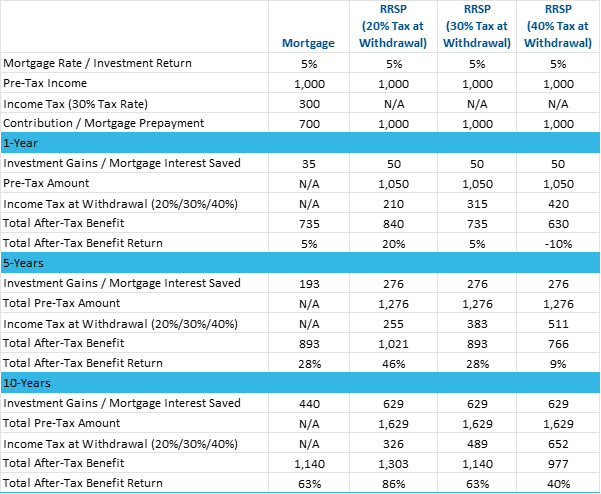

The after-tax return on the RRSP will also depend on the difference between your tax-rate when contributing – or more precisely when you claim the tax deduction from the RRSP contribution – and withdrawing the funds. If these tax rates are the same, the after-tax return will be the same as a TFSA or a mortgage prepayment (see table above). However, if your tax rate is lower at the time of withdrawal, there is the potential for a higher after-tax return, or vice versa, as shown below.

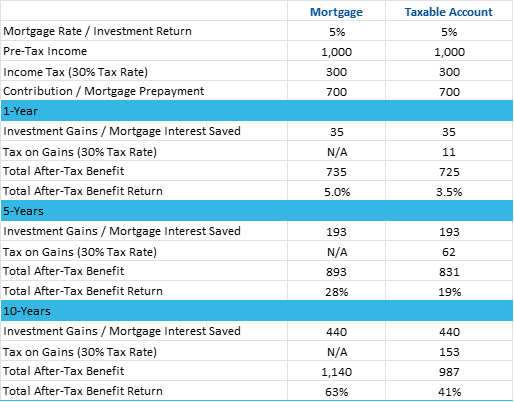

If you have already maximized your TFSA and RRSP contribution room, you may consider investing in a taxable account instead of paying down your mortgage. While a taxable account can also offer the potential for higher returns, better liquidity and diversification, the primary additional drawback when compared to an RRSP or TFSA is the tax considerations.

Any interest income, dividends, or realized capital gains will be taxed in the year they occur. The tax rates can be significant, especially on interest income, which is taxed as regular income at your marginal tax rate. This will lower your after-tax returns and therefore a higher return will be required to equate to paying down your mortgage.

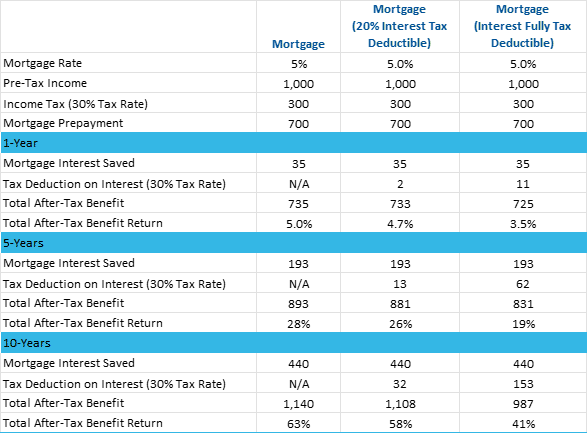

In certain circumstances, mortgage interest can be tax deductible, providing a unique opportunity for tax savings. If you are deducting mortgage interest, it is important to recognize that any prepayments applied to the mortgage will effectively have a lower after-tax benefit.

- Rental Property

If you own a rental property, the interest on your rental property mortgage may be tax-deductible. This can create an incentive to carry a mortgage on your rental property, as the interest expense can offset rental income, reducing your overall taxable income. - Use of Home for Business

If you use your home for your business, you may be able to deduct a portion of your mortgage interest as a business expense. The Canada Revenue Agency (CRA) may allow you to deduct a proportion of your mortgage interest equal to the percentage of your home used for business. For example, if your home office takes up 10% of your home’s square footage and you only use this space for business purposes, you may be able to deduct 10% of your mortgage interest.

In both cases, the potential tax savings could make carrying a mortgage more attractive than paying it down, as the cost of borrowing is effectively reduced. In this instance, your investment returns could be less than the mortgage rate but still equate to the after-tax return from paying down the mortgage.