So far, 2025 has been defined by strong financial market performance despite economic and geopolitical uncertainty. Equity and fixed income investments continue to perform well – buoyed by optimism around Artificial Intelligence (AI), lower interest rates and a resilient economy. Yet this strength has come against a backdrop of elevated valuations, macroeconomic fragility, and heightened geopolitical risks.

While the risk of a broad-scale trade war has receded since Liberation Day last April, instability remains elevated. Tariff levels in the U.S. are still high by historic standards, with significant measures in place against Canada, BRICS nations (Brazil, Russia, India, China and South Africa), and many other countries without a “Deal”. Markets have celebrated the apparent stabilization in trade rhetoric, but the risk of flare-ups persists.

With investors moderating their concerns related to trade and tariffs, the spotlight has returned to AI. AI, and particularly the Large Language Models (LLMs) that power popular chatbots, is undoubtedly an impressive technology. However, it is also extremely capital intensive to build and scale. More users means more data centers, more specialized computing equipment, and more electricity. Many of the leading companies in the space (Microsoft, Google, Meta, Amazon, etc.) have historically had very capital light models. They could scale quickly and efficiently – justifying their elevated valuations. In its current form, AI represents a sharp departure from these capital light business models.

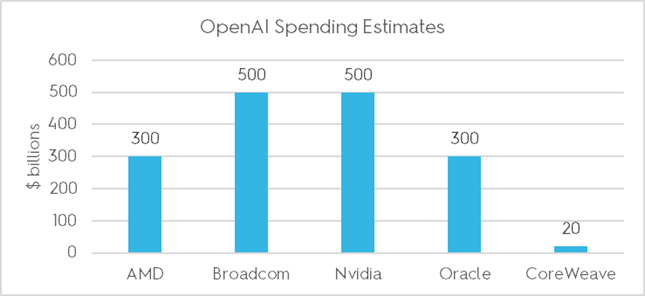

Ever-increasing sums are being funnelled into building data centers and filling them with short-life Graphics Processing Units (GPUs) to train AI models. Most of these GPUs are designed by Nvidia – now the largest company in the world – and all are made in Taiwan – a geopolitical flashpoint. AI spending announcements are reaching astonishing levels with ambitious timelines. OpenAI – the developer of ChatGPT – has been at the center of many of the latest announcements. They have lined up deals to spend more than $1 trillion over the next 5 years. Where this money will come from remains unclear. OpenAI’s annualized revenue is estimated at $13bn – less than 1% of the proposed spending – and it continues to operate at a loss as monetization strategies remain elusive.

Much of the recent investment surge has been financed through debt – vendor credit and private lending, both of which carry higher risks. Vendor financing occurs when suppliers lend directly to their customers. Nvidia, for example, has provided financing and taken equity stakes in other AI-related companies – many of which then use that financing to buy more Nvidia GPUs. This circular flow creates the potential for systemic knock-on effects should any of these companies falter. Private credit, meanwhile, offers very little transparency, making it difficult to assess the true scale of borrowing or potential loss if AI projects fail to deliver.

In addition to AI, the price of gold is another main story for 2025. Gold has reached over $4,200/oz USD – a 60% increase since the start of the year and over doubling since the start of 2024. Gold’s surge has been driven by concerns over inflation, swelling government debt levels, and rising geopolitical tensions. Since Western nations froze Russian central bank assets in 2022, many of the non-Western-aligned central banks have been selling their US asset holdings and accumulating gold reserves instead – over doubling their annual purchases compared to the last decade. As can be seen in the subsequent chart, for the first time since 1996, gold represents a larger share of central banks’ reserves than U.S. Treasuries. Central banks are typically less price sensitive than individual investors – providing support to the ongoing rally. Recent unease over U.S. fiscal stability has only added momentum.

Source: Financial Times

The Canadian Market has been a notable beneficiary of higher gold prices. Despite lackluster economic growth, high unemployment and lingering US tariffs, the TSX has delivered double-digit returns this year. Over half of this performance has come from the materials sector. Many of the TSX-listed gold producers – both large and small – have seen share-price gains exceeding 100% as bullion prices have climbed.

Where do markets go from here? Investors continue to look past risks in search of outsized short-term returns. High valuations and uneven economic fundamentals suggest markets are pricing in a near-perfect scenario – moderating inflation, steady growth and productivity gains from AI. Central banks appear intent on trying to foster this outcome, with both the Bank of Canada and the U.S. Federal Reserve resuming interest-rate cuts. Yet, this is a precarious path. The stimulative power of rate cuts is weaker than in past cycles due to elevated government debt levels. Historically, lower rates boosted the economy through cheaper mortgages. Today, those benefits are more muted, as fiscal deficits keep long-term borrowing costs elevated even as short-term rates fall.

The combination of AI enthusiasm and expectations for easier monetary policy may continue to propel markets – even as valuations stretch further. However, extended periods of optimism often breed complacency – and opportunity for those that are patient. As long-term, disciplined investors, we remain focused on managing risk and preserving capital — realizing gains where prudent and identifying opportunities among quality businesses in less celebrated industries. We believe the long-term risk-reward balance for these companies remains attractive and well aligned with our approach.